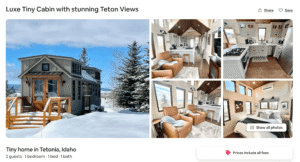

How to Finance a Tiny Home as an Investment Property

Tiny homes have quickly become one of the most dynamic segments in real estate investing. As more people seek flexible, affordable, and eco-conscious housing, the market for tiny homes continues to expand, especially in the short-term rental and vacation space. Investors are taking note, as tiny homes can provide strong returns with lower entry costs than traditional properties. But financing one, particularly as an investment, requires a creative and strategic approach.

This guide explores the different ways to finance a tiny home intended for investment use, with a special look at alternative financing options and how to choose the right lender or builder.

Understanding the Appeal of Tiny Home Investments

The draw of tiny homes as investments comes down to a few key advantages:

- Low capital requirements: Tiny homes typically cost between $75,000 and $175,000, far less than standard residential properties.

- High ROI potential: In the right location, rental income from a tiny home can rival or exceed that of a traditional property.

- Mobility and flexibility: Many tiny homes are on wheels, making it easier to relocate them to high-demand areas or use them seasonally.

- Low maintenance: Smaller spaces mean reduced upkeep costs, both in materials and labor.

Additionally, tiny homes often attract environmentally conscious travelers or renters looking for a unique experience, making them an excellent fit for platforms like Airbnb and VRBO.

Challenges in Financing a Tiny Home

Despite their appeal, tiny homes present a few hurdles when it comes to financing, especially when used as investment properties:

- Not always considered real estate: If the tiny home is on wheels or lacks a permanent foundation, many traditional mortgage lenders won’t classify it as real estate, making it ineligible for a standard home loan.

- Loan size: Because the amounts needed are smaller, some banks or credit unions may not prioritize these loans.

- Zoning and land use: Local regulations can complicate financing and insurance, particularly if the tiny home is used for short-term rentals.

For these reasons, investors often need to look beyond conventional home loans to fund their tiny home projects.

Traditional Financing Options for Tiny Homes

There are a few traditional pathways available for financing a tiny home, though they often depend on whether the home will be stationary or mobile:

Personal Loans

Unsecured personal loans are commonly used for tiny homes. These loans typically offer faster approval, flexible terms, and no requirement for collateral. However, interest rates can be higher compared to secured loans.

RV Loans

If the tiny home is built on a trailer and classified as an RV by the RV Industry Association (RVIA), it may qualify for an RV loan. These loans can offer more favorable terms, but the home must meet specific standards.

Home Equity Loans or HELOCs

For those who already own property, tapping into home equity through a loan or line of credit can be a practical way to finance a tiny home. This option is often preferred due to lower interest rates and longer repayment terms.

Construction Loans

If the tiny home is being built on a permanent foundation, some banks may offer a construction-to-permanent loan. This is more likely if the home will be legally recognized as a dwelling on residential land.

Alternative Financing Options for Tiny Homes

Given the limitations of traditional financing, many investors turn to more flexible, creative solutions to fund their tiny home ventures.

Hard Money Lending

Hard money lenders are private investors or companies that lend based on the value of an asset rather than the borrower’s creditworthiness. These loans can close quickly and are useful for tiny home buyers with bad credit or short-term needs such as construction or flipping.

Peer-to-Peer Lending

Online lending platforms allow individuals to borrow directly from other investors. Sites like Prosper or LendingClub provide access to unsecured loans that can be used for tiny home investments.

Business Loans

If you plan to rent out the tiny home, you may qualify for a small business loan, especially if you structure the investment as a formal entity (like an LLC). SBA microloans or online lenders can provide capital for these projects.

Working with the Right Builder

Partnering with an experienced builder can make a significant difference in your financing journey. Some builders maintain relationships with financing partners or may even offer their own financing options. Look for companies with a track record of helping investors and homeowners navigate zoning, loan requirements, and site planning.

One example is Timbercraft Tiny Homes, a nationally recognized tiny home manufacturer known for premium craftsmanship and design. Timbercraft’s homes are built to high standards, and their team frequently works with clients using a variety of financing approaches, whether the goal is personal use or turning the home into a cash-flowing asset.

Conclusion

Financing a tiny home as an investment property may not follow the same path as traditional real estate, but that doesn’t make it inaccessible. With a clear plan, a flexible mindset, and a willingness to explore alternative lending sources, investors can unlock the full potential of the booming tiny home market.